Soybean oil prices decreased by half in 2025 compared to prices around summertime of 2022. Soybean oil prices hit $0.42 per pound in December 2024, falling from nearly $0.90 per pound as shown in Figure 1. Soybean oil prices remain around $0.45 per pound during 2024 and then rose back to $0.55 per pound by July 2025. Since then, soybean oil dropped down to $0.50 per pound by September 2025.

Soybean meal prices went up and down within the range of $450 to $500 from 2022 to the end of 2023, then consistently dropped to the lowest price ($272) of last five years, in July 2025. Soybean meal price rose slightly to $343 in November 2025, then back to $319 in the first month of 2026, shown in Figure2.

The soybean crush produces two major products: soybean meal and soybean oil. Historically, a little over two thirds of the total value of soybean crush products came from soybean meal and the remaining one third came from soybean oil (before 2021). Prior to 2021, soybean oil began gaining ground on soybean meal. This was primarily due to large increases in the price of soybean oil. Around May 2023, soybean oil prices dropped down, while soybean meal prices gained some ground. This has shifted the relative value of soybean oil down slightly, to around 45% of the value of crush, but soybean oil still makes up a much larger percentage of the total crush value than it historically has, as shown in Figure 3.

At the beginning of 2022, the relative value of soybean meal became greater than the relative value of soybean oil, similar to the relationships of the products before 2021. Around midyear 2022 more seasonality showed up when the relative value of soybean meal went up from 51% at November 2021, to 55% at May 2022, then back to 49% in November 2022. This seesaw pattern in the price of soybean meal continued through the end of 2023. The changes in the relative value of soybean oil changed in the opposite direction as soybean meal did, at the same points in time. For the first half year of 2024, the gap between relative values of soybean oil and soybean meal gets larger, soybean meal reached the highest relative value, to 64%, since 2021, but after July 2024, it dropped down gradually back to 50% level and touched the lowest soybean meal relative value to 48% over the last two decades. Then it went up to 57% in November 2025. A seasonal pattern like the one that appeared in early 2022 may start from then.

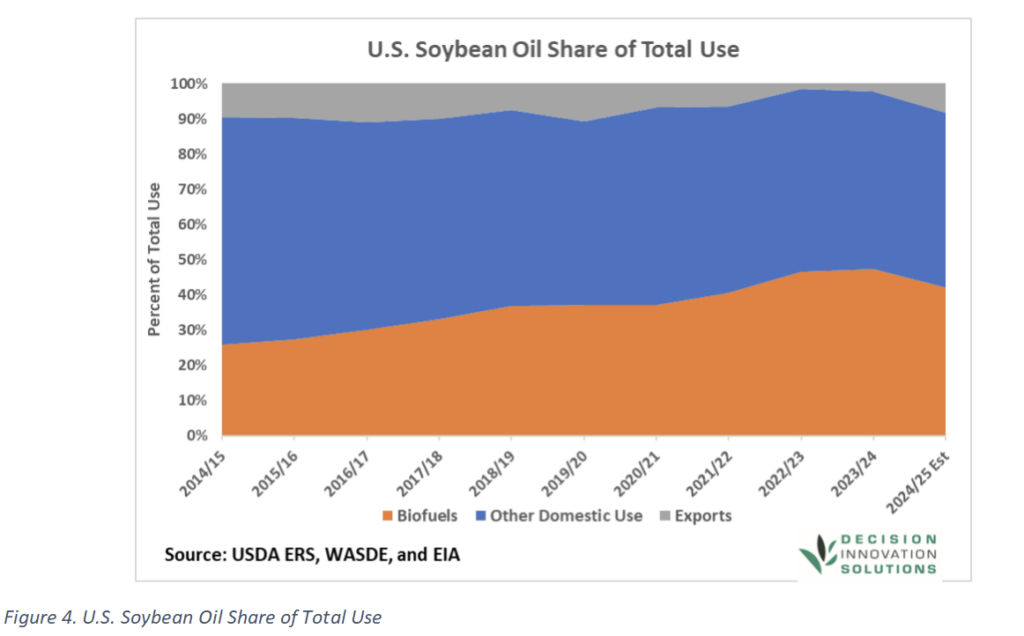

The primary reason for the high price and relative value of soybean oil before 2024 is the increased demand from the biofuels industry. The production of biofuels made from soybean oil as substitutes for diesel fuel are increasing, the most notable being renewable diesel fuel. But after the beginning of fiscal year 2024, the percentage of domestic soybean oil used for biofuels has seen a decreasing trend, from 47% to 43%, shown in Figure 4. Tallow has become one of the top biodiesel inputs. On average, it only occupied 3% of total biodiesel input in 2020. Now about 28% of biodiesel inputs came from tallow in 2025. Although a decrease trend from beef cattle supply has been seen over the last decade, at least for now, inedible tallow production remains at a relatively stable level.

Soybean oil used for biodiesel increased from 7,318 million pounds (59% of total inputs) to its highest point of 13,320 million pounds (35% of total input) from 2019 to 2024, then fell slightly back to 11,182 million pounds in 2025, as shown in Figure 5. Note that, when writing this article, EIA had not yet published the data for November and December in 2025, so it was assumed to be the same as it in October 2025.

Soybean crush is expected to increase in the coming years with much of this increase in domestic crush driven by a desire to have more soybean oil available for domestic biofuel production. Including expansions and new plants, the American Soybean Association announced in 2025, 75 million bushels per year of capacity came online and another 114 million bushels will be coming in 2026. By the end of 2026, total crush capacity could reach nearly 2,740 million bushels per year.

Renewable diesel will likely provide additional demand for additional soybean oil, but tallow could be a strong competitor to soybean oil. Renewable diesel production saw a slight decrease from 2025, possibly Due to a policy change with regards to biodiesel tax credits. Also, the market for additional soybean meal produced has not yet been realized. Domestically, most soybean meal is fed to livestock. Although the soybean meal consumption could rise in poultry, and some growth phases for swine, large growth in U.S. livestock numbers is not expected in the coming years. A failure to effectively market new soybean meal could lead to depressed soybean meal prices, which could depress the price of other commodities, including soybeans, corn DDGs, and some rendered animal proteins, particularly meat and bone meal and poultry byproduct meal.